Maximizing Your Tax Refund: Tips and Tricks for a Bigger Return

Tax refunds are an important aspect of the tax system that many individuals eagerly anticipate each year. A tax refund is essentially a reimbursement from the government for any excess taxes that you have paid throughout the year. It is a way for the government to return money to taxpayers who have overpaid their taxes. In this article, we will explore various strategies and tips to help you maximize your tax refund. By understanding the basics of tax refunds, utilizing deductions and credits, keeping accurate records, filing at the right time, taking advantage of charitable giving, retirement planning, homeownership benefits, education tax breaks, and business deductions, you can ensure that you are getting the most out of your tax return.

Key Takeaways

- A tax refund is money returned to you by the government if you overpaid your taxes.

- Your tax refund is calculated based on your income, deductions, and credits.

- Keeping accurate records and proper documentation is crucial for maximizing your tax refund.

- Filing your taxes at the right time and taking advantage of charitable giving, retirement contributions, homeownership benefits, and education tax breaks can all increase your refund.

- Business owners and self-employed individuals should take advantage of deductions and credits to maximize their refund, while avoiding common tax mistakes can help you keep more of your money.

Understanding the Basics: What is a Tax Refund and How is it Calculated?

A tax refund is a reimbursement from the government for any excess taxes that you have paid throughout the year. When you file your tax return, you calculate your total income and subtract any deductions and credits that you are eligible for. The resulting amount is your taxable income, on which you owe taxes. If you have already had taxes withheld from your paycheck throughout the year, this amount will be subtracted from your total tax liability. If the amount withheld is greater than your total tax liability, you will receive a refund for the excess amount.

To calculate your tax refund, you need to accurately report your income and deductions on your tax return. This means keeping track of all sources of income, such as wages, self-employment income, rental income, and investment income. It also means accurately reporting any deductions or credits that you are eligible for, such as mortgage interest deductions, student loan interest deductions, or child tax credits.

Filing an accurate tax return is crucial because any errors or omissions can result in penalties or delays in receiving your refund. It is important to keep all necessary documentation and receipts to support your claims and ensure that you are eligible for the deductions and credits you are claiming.

Deductions and Credits: Maximizing Your Refund Through Smart Tax Planning

Deductions and credits are two key ways to maximize your tax refund. Deductions reduce your taxable income, while credits directly reduce the amount of tax you owe. By taking advantage of these deductions and credits, you can lower your tax liability and potentially increase your refund.

There are numerous deductions and credits available to taxpayers, depending on their individual circumstances. Some common deductions include mortgage interest, state and local taxes, medical expenses, and student loan interest. These deductions can significantly reduce your taxable income and increase your refund.

Similarly, there are various tax credits available that can directly reduce the amount of tax you owe. Some common credits include the Earned Income Tax Credit (EITC), Child Tax Credit, and American Opportunity Credit for education expenses. These credits can provide a dollar-for-dollar reduction in your tax liability, resulting in a larger refund.

To maximize your deductions and credits, it is important to keep accurate records and stay informed about changes in tax laws. By staying organized and keeping track of all relevant receipts and documentation, you can ensure that you are claiming all eligible deductions and credits. Additionally, staying up to date with changes in tax laws can help you take advantage of new deductions or credits that may be available to you.

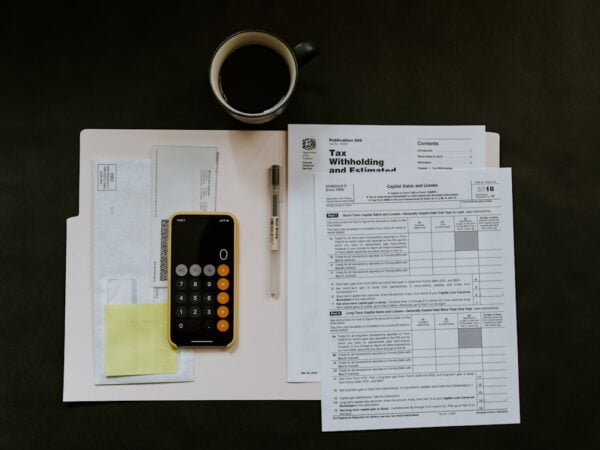

Keeping Accurate Records: Why Proper Documentation is Key to a Bigger Return

| Metrics | Description |

|---|---|

| Increased Efficiency | Proper documentation helps in streamlining processes and reduces the time and effort required to retrieve information. |

| Improved Decision Making | Accurate records provide valuable insights and data that can be used to make informed decisions and improve business operations. |

| Compliance | Proper documentation ensures compliance with legal and regulatory requirements, reducing the risk of penalties and fines. |

| Reduced Errors | Accurate records reduce the risk of errors and mistakes, which can lead to costly rework and damage to the company’s reputation. |

| Cost Savings | Proper documentation can help in identifying areas of inefficiency and waste, leading to cost savings and increased profitability. |

Keeping accurate records is crucial when it comes to maximizing your tax refund. Proper documentation ensures that you have the necessary evidence to support your claims for deductions and credits. Without proper documentation, you may not be able to claim certain deductions or credits, resulting in a smaller refund.

There are several types of records that you should keep to support your tax return. These include:

– Income records: Keep copies of all W-2 forms, 1099 forms, and any other documents that show your income for the year. This includes income from employment, self-employment, rental properties, and investments.

– Expense records: Keep receipts, invoices, and other documentation for any expenses that you plan to deduct. This includes expenses related to business, education, medical costs, and charitable donations.

– Investment records: Keep records of any buying or selling of stocks, bonds, or other investments. This will help you accurately report any capital gains or losses on your tax return.

– Homeownership records: If you own a home, keep records of mortgage interest payments, property taxes paid, and any home improvements or repairs that may be deductible.

By keeping accurate records throughout the year, you can ensure that you have all the necessary documentation to support your claims on your tax return. This will help you maximize your deductions and credits and potentially increase your refund.

Timing is Everything: Strategies for Filing at the Right Time to Boost Your Refund

The timing of when you file your taxes can have an impact on the size of your refund. There are benefits to both filing early and filing late, depending on your individual circumstances.

Filing early can be beneficial if you are expecting a refund. By filing early, you can receive your refund sooner and put the money to use. This can be especially helpful if you have plans for the money, such as paying off debt or making a large purchase. Additionally, filing early can help protect against identity theft. By filing early, you reduce the risk of someone else filing a fraudulent return using your information.

On the other hand, filing late can be beneficial if you owe taxes. By waiting until the last minute to file your taxes, you have more time to gather all necessary documentation and ensure that your return is accurate. Additionally, if you owe taxes and cannot pay the full amount by the filing deadline, you may be able to set up a payment plan with the IRS. This can help alleviate the financial burden of paying a large tax bill all at once.

Ultimately, the best time to file your taxes depends on your individual circumstances. If you are expecting a refund and have all necessary documentation, filing early may be the best option. If you owe taxes and need more time to gather documentation or set up a payment plan, filing closer to the deadline may be the best choice.

The Importance of Charitable Giving: How Donations Can Help You Save on Taxes

Charitable giving is not only a way to support causes that are important to you, but it can also provide tax benefits. Donations to qualified charitable organizations can be deducted from your taxable income, potentially increasing your refund.

There are several types of charitable donations that can increase your refund. Cash donations are the most common and can include donations made by check, credit card, or electronic transfer. Non-cash donations, such as clothing, furniture, or household items, can also be deducted if they are in good condition and donated to a qualified organization.

To maximize your tax benefits from charitable giving, it is important to keep accurate records of your donations. This includes keeping receipts or acknowledgments from the charitable organization that show the date and amount of your donation. Additionally, if you make non-cash donations, you should keep a detailed list of the items donated and their fair market value.

By taking advantage of the tax benefits of charitable giving, you can support causes that are important to you while also potentially increasing your tax refund.

Retirement Planning: Using Contributions to Retirement Accounts to Lower Your Tax Bill

Contributions to retirement accounts can provide significant tax benefits and potentially increase your refund. By contributing to retirement accounts such as a 401(k) or IRA, you can lower your taxable income and potentially qualify for additional tax credits.

Contributions to traditional retirement accounts are typically made with pre-tax dollars, meaning they are deducted from your taxable income. This can lower your overall tax liability and potentially increase your refund. Additionally, contributions to certain retirement accounts, such as a Roth IRA, may be eligible for the Retirement Savings Contributions Credit, also known as the Saver’s Credit. This credit can provide a dollar-for-dollar reduction in your tax liability, resulting in a larger refund.

To maximize your tax benefits from retirement contributions, it is important to contribute the maximum amount allowed by law. Additionally, it is important to keep accurate records of your contributions and any applicable tax forms, such as Form 5498 for IRA contributions.

By taking advantage of the tax benefits of retirement contributions, you can lower your tax bill and potentially increase your refund.

Homeownership Benefits: How Owning a Home Can Increase Your Refund

Owning a home can provide several tax benefits that can increase your refund. Mortgage interest deductions and property tax deductions are two common deductions that homeowners can take advantage of.

Mortgage interest deductions allow homeowners to deduct the interest paid on their mortgage from their taxable income. This can significantly reduce your overall tax liability and potentially increase your refund. Additionally, property tax deductions allow homeowners to deduct the amount paid in property taxes from their taxable income.

To maximize your tax benefits from homeownership, it is important to keep accurate records of mortgage interest payments and property tax payments. Additionally, it is important to ensure that you are eligible for these deductions based on the requirements set forth by the IRS.

By taking advantage of the tax benefits of homeownership, you can potentially increase your refund and reduce your overall tax liability.

Education Tax Breaks: Taking Advantage of Credits and Deductions for Education Expenses

Education expenses can provide several tax benefits that can increase your refund. There are several credits and deductions available for education expenses, depending on your individual circumstances.

The American Opportunity Credit is a tax credit that can provide up to $2,500 per eligible student for qualified education expenses. This credit is available for the first four years of post-secondary education and can provide a dollar-for-dollar reduction in your tax liability.

The Lifetime Learning Credit is another tax credit that can provide up to $2,000 per tax return for qualified education expenses. This credit is available for an unlimited number of years and can also provide a dollar-for-dollar reduction in your tax liability.

In addition to these credits, there are also deductions available for education expenses. The Tuition and Fees Deduction allows taxpayers to deduct up to $4,000 in qualified education expenses from their taxable income.

To maximize your tax benefits from education expenses, it is important to keep accurate records of all education-related expenses. This includes tuition payments, books, supplies, and any other expenses that may be eligible for a deduction or credit.

By taking advantage of the tax benefits of education expenses, you can potentially increase your refund and reduce your overall tax liability.

Business Owners and Self-Employed Individuals: Tips for Maximizing Your Refund

Business owners and self-employed individuals have unique opportunities to maximize their tax refund through various deductions and credits. By understanding the specific tax benefits available to them, they can potentially increase their refund and reduce their overall tax liability.

Some common deductions for business owners and self-employed individuals include home office deductions, vehicle expenses, business travel expenses, and health insurance premiums. These deductions can significantly reduce your taxable income and potentially increase your refund.

Additionally, there are several credits available to business owners and self-employed individuals. The Small Business Health Care Tax Credit is a credit that can help small businesses afford health insurance coverage for their employees. The Self-Employment Tax Deduction allows self-employed individuals to deduct a portion of their self-employment taxes from their taxable income.

To maximize your tax benefits as a business owner or self-employed individual, it is important to keep accurate records of all business-related expenses. This includes receipts, invoices, and any other documentation that supports your claims for deductions or credits.

By taking advantage of the tax benefits available to business owners and self-employed individuals, you can potentially increase your refund and reduce your overall tax liability.

Avoiding Common Tax Mistakes: How to Stay on the IRS’s Good Side and Keep More of Your Money

Avoiding common tax mistakes is crucial when it comes to maximizing your tax refund. Making errors or omissions on your tax return can result in penalties or delays in receiving your refund. By staying informed and seeking professional help when needed, you can ensure that you are filing an accurate and complete tax return.

Some common tax mistakes to avoid include:

– Failing to report all sources of income: It is important to accurately report all sources of income on your tax return. This includes income from employment, self-employment, rental properties, and investments.

– Forgetting to claim deductions or credits: It is important to take advantage of all deductions and credits that you are eligible for. This includes deductions for mortgage interest, student loan interest, and medical expenses, as well as credits for education expenses and child care expenses.

– Filing with incorrect information: It is important to double-check all information on your tax return before filing. This includes ensuring that your name, Social Security number, and other personal information are correct.

– Failing to keep accurate records: Keeping accurate records is crucial when it comes to supporting your claims for deductions and credits. Without proper documentation, you may not be able to claim certain deductions or credits.

– Not seeking professional help when needed: If you have complex tax situations or are unsure about certain aspects of your tax return, it is important to seek professional help. A tax professional can help ensure that you are filing an accurate and complete tax return.

By avoiding common tax mistakes and filing an accurate and complete tax return, you can stay on the IRS’s good side and potentially increase your refund.

Tax refunds are an important aspect of the tax system that can provide a financial boost for individuals each year. By understanding the basics of tax refunds, utilizing deductions and credits, keeping accurate records, filing at the right time, taking advantage of charitable giving, retirement planning, homeownership benefits, education tax breaks, and business deductions, you can ensure that you are getting the most out of your tax return. By following these tips and strategies, you can maximize your refund and keep more of your hard-earned money.

If you’re eagerly awaiting your tax refund, you might also be interested in exploring ways to improve your overall well-being. Check out this article on “Small Changes, Big Results: Easy Habits for a Healthier You” from Wave Magnets. It offers practical tips and habits that can have a significant impact on your physical and mental health. From incorporating exercise into your routine to making healthier food choices, these simple changes can lead to big results. So while you’re waiting for that refund, why not invest in yourself and start building healthier habits? Read more

FAQs

What is a tax refund?

A tax refund is a reimbursement of excess taxes paid to the government by an individual or business.

How do I know if I am eligible for a tax refund?

You may be eligible for a tax refund if you have overpaid your taxes or if you are eligible for tax credits or deductions.

How do I apply for a tax refund?

To apply for a tax refund, you need to file a tax return with the government. You can file your tax return online or by mail.

How long does it take to receive a tax refund?

The time it takes to receive a tax refund varies depending on the government agency and the method of filing. Generally, it takes around 2-3 weeks for an e-filed tax return to be processed and for the refund to be issued.

What happens if I made a mistake on my tax return?

If you made a mistake on your tax return, you can file an amended tax return to correct the error. This may delay the processing of your refund.

Can I receive my tax refund via direct deposit?

Yes, you can choose to receive your tax refund via direct deposit into your bank account. This is often the fastest and most secure way to receive your refund.

What should I do if I haven’t received my tax refund?

If you haven’t received your tax refund within the expected timeframe, you should contact the government agency responsible for processing your tax return. They can provide you with an update on the status of your refund.